Who is eligible to apply?

Eligible applicants are required to demonstrate that their organisation is a genuine social enterprise by providing evidence of one or more of the following:

- Social Traders certification* (For Social Enterprise | Social Traders)

- People and Planet First (PPF) verification* (Verification | QSEC)

- Registration via the Office of the Registrar of Indigenous Corporations or certification with Supply Nation, and ability to demonstrate how they deliver outcomes as part of their business operations.

*If your organisation is proposing to obtain Social Traders certification or PPF verification, there is opportunity to note this in your application. Certification or verification does not need to be finalised for consideration of Stage 1 applications, provided the application to obtain certification or verification has commenced.

Eligible applicants must also be:

- operating in Queensland with a physical presence in Queensland

- generating or will be generating (within a year of contract commencement) a social benefit which occurs in Queensland

- able to demonstrate potential for sustainable growth in trade revenue and social impact. (This might be demonstrated, for instance, through a history of trade revenue growth or by having secured investment, land or other capital that is expected to unlock trade revenue growth within a year of contract commencement, and be profitable or the potential to be profitable)

- able to demonstrate good governance by having an established independent board in place or by providing a method statement that demonstrates transparent, accountable and effective decision

making structures that balance social mission, financial sustainability, and stakeholder interests. (For detail on what comprises an adequate ‘method statement’, see further FAQs below).

Can individuals apply for an Impact Revenue Investment?

No, to apply you must be a social enterprise aligned to the eligibility requirements above.

I’m a Not-for-Profit organisation can I apply for an Impact Revenue Investment?

If you can demonstrate that your organisation is a social enterprise (as defined above), then you can apply for an Impact Revenue Investment. This includes social enterprises that are subsidiaries of not-for-profit organisations.

If your not-for-profit organisation is not currently operating a social enterprise, but is looking to expand existing activities to include social enterprise, you are not eligible for this round of Impact Revenue Investments.

What are the social impact priority areas that the Office of Social Impact (OSI) is most interested in funding?

OSI is particularly interested in supporting organisations that deliver measurable social impact in the following areas:

- Quality jobs for disadvantaged Queenslanders: Supporting projects that create sustainable employment opportunities for individuals facing barriers to workforce participation.

- Supporting marginalised young people: Supporting young people and their families to thrive, making communities safer, reducing the number of children and young people in out-of-home care, and improving outcomes for those in care, by addressing root causes and fostering positive pathways.

- Reducing addiction and improving mental health: Initiatives that tackle substance abuse, promote mental health, and provide accessible support services.

- Improving women’s safety and preventing domestic and family violence (DFV): Social enterprises that support people impacted by DFV, enhance safety for women, and address the underlying causes of DFV.

- Increasing social and affordable housing: Projects that expand access to safe, affordable, and inclusive housing.

- Creating place-based initiatives: Supporting community-driven solutions that enable all communities to thrive by addressing local challenges and opportunities.

OSI will also consider applications with potential for high impact in other social areas.

If my organisation doesn’t specifically support one of the priority areas listed above, am I still eligible?

Yes. While these areas are priorities, consideration will also be given to other high-impact initiatives that demonstrate strong potential to deliver positive and measurable social outcomes in Queensland. If your organisation addresses other critical social needs in Queensland, we encourage you to apply and outline the impact you aim to achieve.

Is there a preference for social enterprises to scale their existing impact, or is expanding into new areas relevant?

As long as the organisation meets the eligibility criteria and the impact is going to be delivered in Queensland, there is no preference for scaling current activities over expanding into new areas, locations

or activities.

However, organisations will need to demonstrate how the government support will enable their enterprise to grow its trading revenue and move towards financial sustainability, in order to achieve greater social impact.

What can and can’t the funding be used for?

Government funding provided through the impact revenue investment product is untied, offering maximum flexibility to support your organisation’s needs. You can allocate the funding towards any operational or capital expenses that will help achieve your organisation’s goals and amplify its impact. Examples include:

- salaries and wages for staff

- professional services such as accounting, legal, or marketing support

- administrative costs like rent, utilities, or insurance

- technology upgrades, software, or equipment to improve efficiency

- purchasing or upgrading physical assets, such as buildings, vehicles, or machinery

- developing infrastructure to support service delivery or business growth

- investing in tools or resources to enhance your organisation’s capacity.

You cannot however use the funding for a private benefit, such as excessive remuneration or dividends, purchase or improvement of assets for primarily private use, or the use of funds to increase private business value.

What documentation do I need to attach to my Stage 1 application?

If you have an independent board, you will not be required to submit any documentation.

If you do not have an independent board, you will be required to attach a method statement about your organisation’s governance. Refer to the next FAQ for a detailed description of what to include in your method statement.

What do you mean by ‘operating model’ and how are the various models defined?

An operating model refers to the framework or approaches your organisation uses to deliver its services, achieve its objectives, and manage resources. Types of operating models include:

- Work integrated social enterprise: Creates employment and training opportunities for marginalised people.

- Community need: Delivers accessible products and services to meet community needs that are not met by the market.

- Profit redistribution: Donates at least 50% of profits or revenue to charity.

How does the two-stage assessment process work?

In Stage 1, applicants need to provide basic information about their organisation, including its financial history, potential for revenue growth, and its social impact areas. This information will be submitted without supporting evidence for the purpose of Stage 1 and will be assessed against the criteria outlined in the Guidelines. Applicants who are shortlisted in Stage 1 will be invited to submit an application in Stage 2.

In Stage 2, applicants will be asked to provide additional details and evidence to support the claims made in Stage 1. This could include documents like financial statements, impact assessments, or certifications, as well as other information and evidence to inform the assessment of your organisational capability, financial viability, revenue growth potential and social impact quality. The Stage 2 assessment will use this evidence, along with the Stage 1 information, to decide which applications will be recommended for funding.

What support is available during the application process?

OSI will provide:

If I’m successful in both Stage 1 and 2, how onerous are the reporting requirements for this program?

Trading revenue will need to be reported every 6 months to determine how much funding you are eligible to receive under the IRI program, and audited financial accounts provided annually.

You will also be required to report every 6 months on the social impact that your organisation has created in Queensland as a result of the government support, however, government payments will be made on the basis of revenue growth not social impact.

More information will be provided to applicants who are invited to apply to Stage 2.

If I am successful, how many years of funding support do I receive?

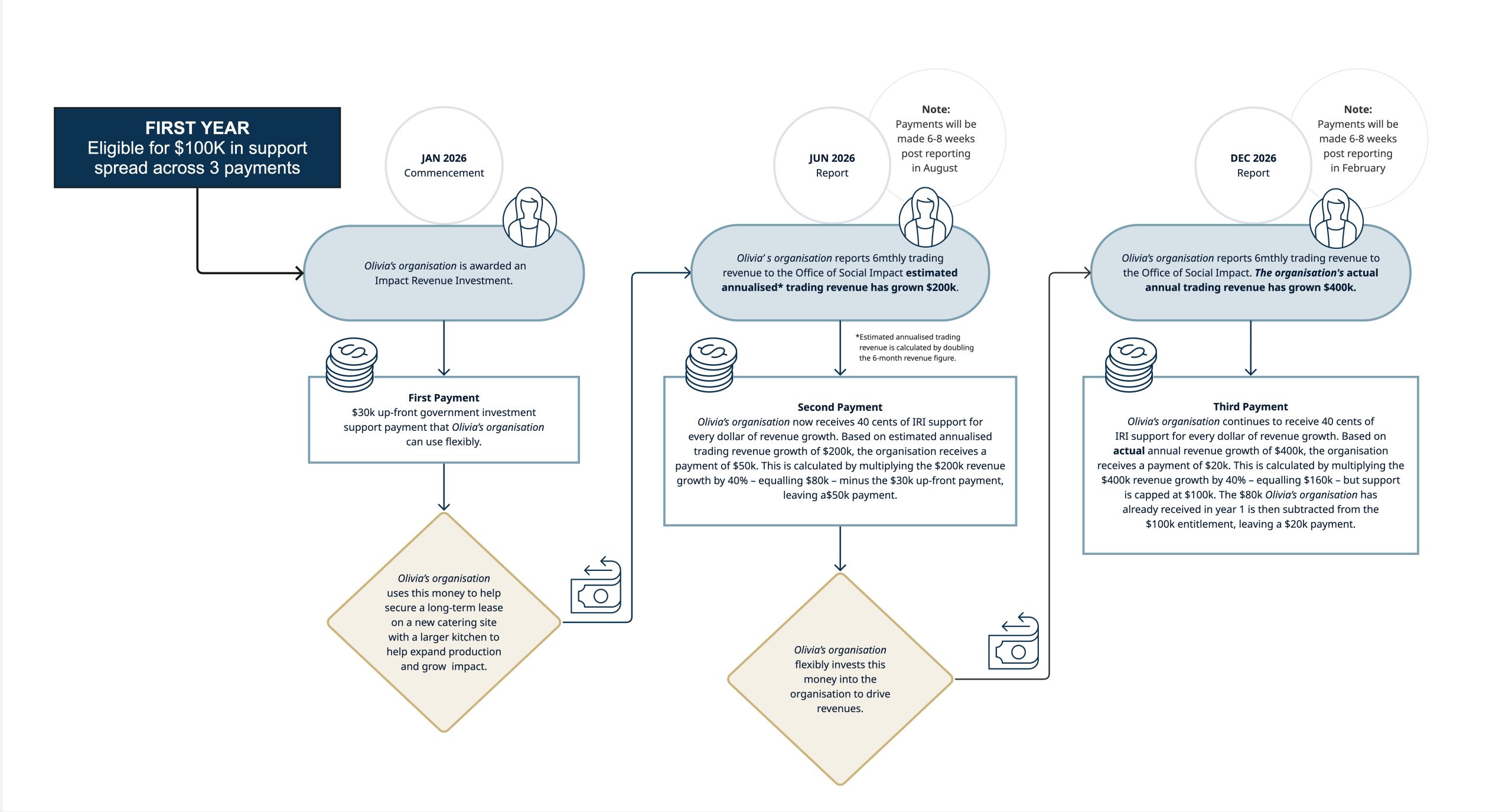

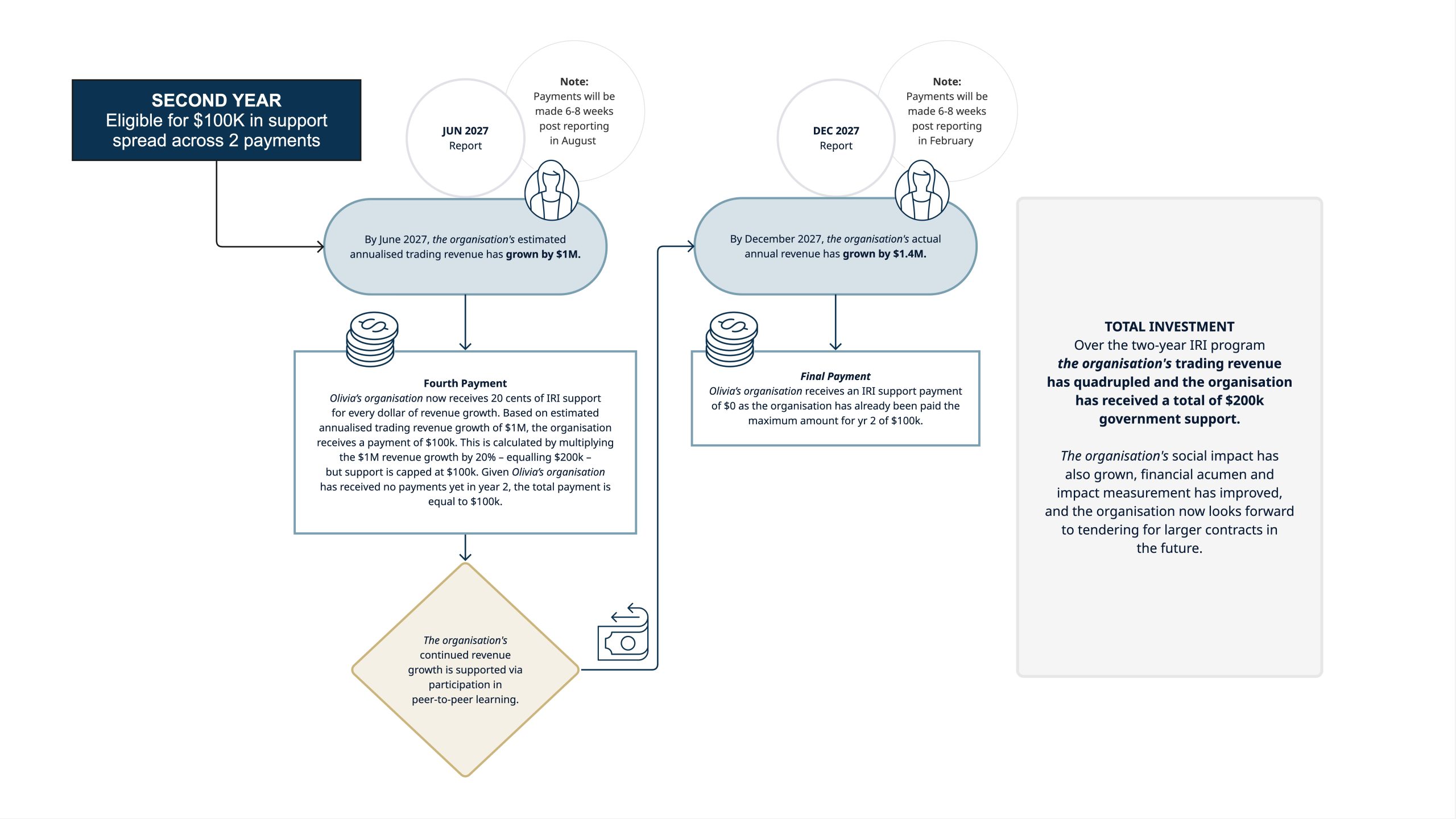

Successful social enterprises will be eligible for two years of IRI support capped at $100,000 in the first year and $100,000 in the second year (or a total of $200,000 over two years). The total amount you will be entitled to however will depend on the growth in trading revenue earned. See further below for more detail.

How much government funding am I likely to receive under the IRI program and over what time period?

Eligible social enterprises can receive up to $100,000 in the first year (inclusive of a $30,000 upfront payment) and up to $100,000 in the second year (there is no upfront payment in the second year).

The total funding you are entitled to in each year is tied to your trading revenue growth, with funding calculated at a rate of $4.00 for every $10.00 growth in trading revenue in the first year tapering to $2.00 for every $10.00 growth in trading revenue in the second year. For further detail around how individual payments are calculated, refer to the ’How do IRIs work in practice’ below.

Is there any funding support provided up-front?

Yes, 30% of the first year’s funding ($30,000 per year) will be paid upfront, with the remainder distributed in six-monthly payments across the two-year program subject to and based on demonstrated growth in trading revenue.

Subsequent payments in the first year will factor in the $30,000 upfront payment to avoid over payment. For further detail around how individual payments are calculated, refer to the ’How do IRIs work in practice’ below.

Will any non-financial support be provided?

Yes, non-financial support will be provided as part of the IRI program to ensure social enterprises have access to both the financial and non-financial support necessary to succeed.

This will include peer-to-peer learning opportunities. This will enable participants to share experiences, insights, and best practices with others in the sector, creating a supportive network for mutual growth and learning.

Will there be any future rounds of IRIs?

Yes, the intention is to run three rounds of IRIs, with applications opening in 2025, 2026 and 2027 for commencement in the subsequent year.

OSI reserves the right to alter the eligibility criteria, application process and priority focus areas for future rounds.

What happens if our application is unsuccessful?

Unsuccessful applicants will be notified following both the Stage 1 and Stage 2 assessment process.

How do IRIs work in practice?

CASE STUDY: Olivia’s Catering

Olivia’s Catering is an organisation in Ipswich that employs disadvantaged Queenslander’s who are struggling to enter the job market. The organisation provides employees with on-the-job training to help them build transferable employment skills in the areas of hospitality, catering and customer service and connects employees with wrap-around social support services such as housing and psychological support to help them thrive in paid employment.

Olivia’s organisation:

- currently earns $600k in trading revenue each year, with all profits re-invested to grow her social impact

- has the opportunity to quadruple trading revenue over the next two years but requires investment to expand

- has accreditation with both Social Traders and People and Planet First and operates with an independent board

- as a social enterprise that delivers impact in Queensland and with strong growth potential, Olivia’s organisation is successfully awarded the 2-year Impact Revenue Investment funding support from the Queensland Government.

View the IRI payment schedule for the first year.

View the IRI payment schedule for the second year.

{kind=link}

{kind=link}